The Market Just Split in Half. Here's Which Side You're On.

Zillow released data this week confirming what our Q1 numbers in Roscommon County already show: there are two housing markets operating right now — not two different towns, not two different price ranges — two lanes running side by side in the same ZIP codes. One lane moves fast and rewards sellers. The other sits, bleeds leverage, and costs real money.

What Zillow Found Nationally

Zillow's February 2026 analysis of national home sales identified a clear split in how listings are behaving. Roughly 18.5 percent of homes went under contract within the first seven days of listing. That segment — the fast movers — performed dramatically better than everything else. Homes that went pending within a week were 2.6 times more likely to close above asking price. Among those fast-moving listings, 44 percent sold above list price. Among all homes? Only 17 percent did.

The other side of that equation is just as telling. The typical home that sold went pending in 19 days. The median active listing — the ones still sitting — had been on the market 56 days. That gap between how quickly sold homes moved versus how long unsold listings had been sitting reached its widest point for any March since 2020. Zillow described it plainly: buyers now have more choices and more leverage than they've had in years, and homes that stand out get rewarded while others wait.

That's the national picture. Here's the local one.

Our Q1 Numbers Tell the Same Story

Roscommon County closed Q1 2026 with 67 sales, $14.9 million in volume, and 1.91 months of supply countywide. Supply is still tight. The seller's market backbone is still intact. But the headline hides what's actually happening inside the data.

Sixteen of those 67 closings — nearly one in four — took 121 days or more to sell. That's not bad luck. That's overpricing compounding into lost time and lost negotiating position.

The most dramatic example is Houghton Lake waterfront. Median sold price on waterfront actually rose quarter-over-quarter — from $385,000 to $572,250 — because the handful of sales that did close concentrated into higher-ticket product. But sold-to-list-price collapsed from 96.25 percent to 85.51 percent. That means buyers on Houghton waterfront in Q1 weren't paying more than last year's buyers — they were extracting the biggest discounts we've seen in that segment in recent memory. The price went up on paper. The negotiating leverage went to the buyer. Those are not the same thing, and too many sellers treat them as if they are.

On the other end of the county, 48629 — the Houghton Lake non-waterfront ZIP — compressed to 1.48 months of supply, the sharpest inventory tightening in the full data set. The market didn't go soft. Buyers just got selective. When the price was right, they moved. When it wasn't, they walked.

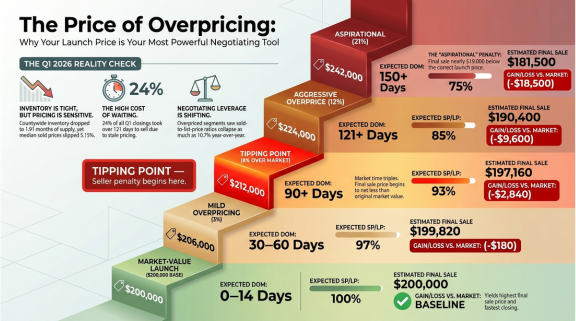

The Penalty Is Not Abstract — It's Quantifiable

The diagram above maps exactly what overpricing costs in this market. It's not a theory. It's arithmetic.

A property priced at market value — the $200,000 baseline in this model — goes under contract in 14 days or less, sells at 100 percent of asking, and yields the highest net to the seller. Move that same property into mild overpricing territory, and you're looking at 30 to 60 days on market and 97 cents on the dollar. Push it to 6 percent over market and you've crossed the tipping point — market time triples, and the final sale price begins to net less than the original market value. Full aspirational pricing, 21 percent over market? You're looking at 150 or more days on market, a 75 percent sold-to-list ratio, and a final sale price that comes in roughly $18,500 below where a market-value launch would have gotten you on day one.

The sellers who got hurt in Q1 weren't in a bad market. They were in the wrong lane of a good one.

What This Means If You're Selling

Low supply is still your friend — but it is not a blank check. The market does not reward listing price. It rewards value. The buyers who are active right now are financially sophisticated, often pre-approved at tight debt-to-income ratios, and they have enough inventory to be selective. They are not desperate. They will not overpay to compete for a listing that's already been sitting for 45 days. The window where overpriced listings still sold — just slower — has narrowed significantly.

Correct pricing at launch is the most powerful negotiating tool available to a seller right now. Not the most comfortable decision. The most effective one.

What This Means If You're Buying

The Zillow data makes this point clearly: buyers have more options and more negotiating leverage right now than at any point since before the pandemic. In specific segments — including Houghton waterfront, overbuilt non-waterfront listings in 48656, and anything that's been sitting past 90 days — the leverage is real and available to a buyer who knows how to use it. That requires an agent who understands the local data well enough to identify which listings are priced correctly and which ones are sitting because the math doesn't support the ask.

There are opportunities in this market. They're just not where the listing price says they are.

Bottom Line

The Northern Michigan market is not soft. Supply is still tight. Demand is still present. But the market has stopped carrying overpriced listings on goodwill. The data from Q1 is clear, and Zillow's national analysis confirms it's not a local anomaly. There are two lanes. Which one your property ends up in is largely a pricing decision — and that decision happens before the sign goes in the yard.

If you're thinking about listing this spring or summer, let's look at the actual numbers for your property before we talk price. That conversation is free. The alternative isn't.